The latest development in insurance technology (Insurtech) is the rise of Peer to peer Insurance. The idea of peer to peer insurance is to form a reciprocity insurance contract through the Collaborative consumption concept.

Collaborative consumption (CC) can be defined as the set of resource circulation systems, which enable consumers to both "obtain" and "provide", temporarily or permanently, valuable resources or services through direct interaction with other consumers or through a mediator (Ertz, et.al: 2016).

Direct interaction can done through digital platform or known as P2P Platform, empowering the use of internet network.

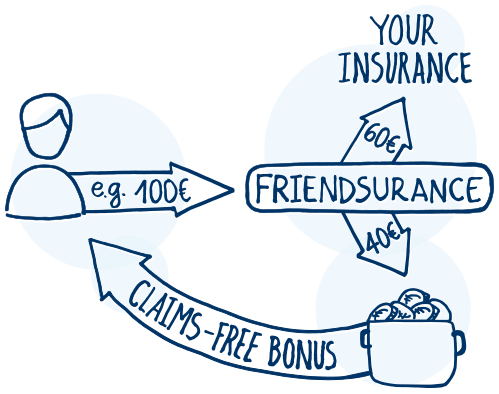

By doing benchmarking to one of the well known peer to peer insurance startups (www.friendsurance.com), P2P insurance works based on a shareconomy approach, policy owners with the same insurance type form small groups. A part of their premiums is paid into a cashback pool. If no claims are submitted, the members of the group get some of their money back at the end of the year. In case of claims, the cashback decreases for everyone. Small claims are settled with the money in the pool. In the event of bigger claims, the standard insurance company covers any amount that exceeds the coverage through the group. In case there is insufficient money left in the pool to cover a claim, a stop-loss insurance covers the rest. As a result, policy owners always enjoy full coverage and never pay more than they would.

If we observed closely, there are similarities between the peer to peer insurance concept with takaful insurance concept, that is in the form of Risk Sharing. In conventional insurance, the concept is Risk Transfer.

In takaful insurance concept, the Insurance contribution (or in the conventional insurance is called, premium) are divided to Tabarru (Risk fund pool) and Ujroh (operators fee / Wakala Fee). The basis of the operation is "Ta'awun", meaning 'Helping each others'.

The Tabarru is what the operator use to pay for the participant claims. If the Tabarru funds have a profit, than participants will have the right to a profit sharing, usually used as renewal discount. The operator will take their operational fees only from the Ujroh fund.

So it seems that how the P2P Insurance works is similar to takaful insurance process. Takaful insurer should optimize and be the party that takes the most benefit from the rise of P2P platform to further expand their business, because from the process point of view it is already a match.

If we observed closely, there are similarities between the peer to peer insurance concept with takaful insurance concept, that is in the form of Risk Sharing. In conventional insurance, the concept is Risk Transfer.

In takaful insurance concept, the Insurance contribution (or in the conventional insurance is called, premium) are divided to Tabarru (Risk fund pool) and Ujroh (operators fee / Wakala Fee). The basis of the operation is "Ta'awun", meaning 'Helping each others'.

The Tabarru is what the operator use to pay for the participant claims. If the Tabarru funds have a profit, than participants will have the right to a profit sharing, usually used as renewal discount. The operator will take their operational fees only from the Ujroh fund.

So it seems that how the P2P Insurance works is similar to takaful insurance process. Takaful insurer should optimize and be the party that takes the most benefit from the rise of P2P platform to further expand their business, because from the process point of view it is already a match.